Spoiler alert: Not as much as you might think. Here’s why you should save now instead of worrying about financial aid later.

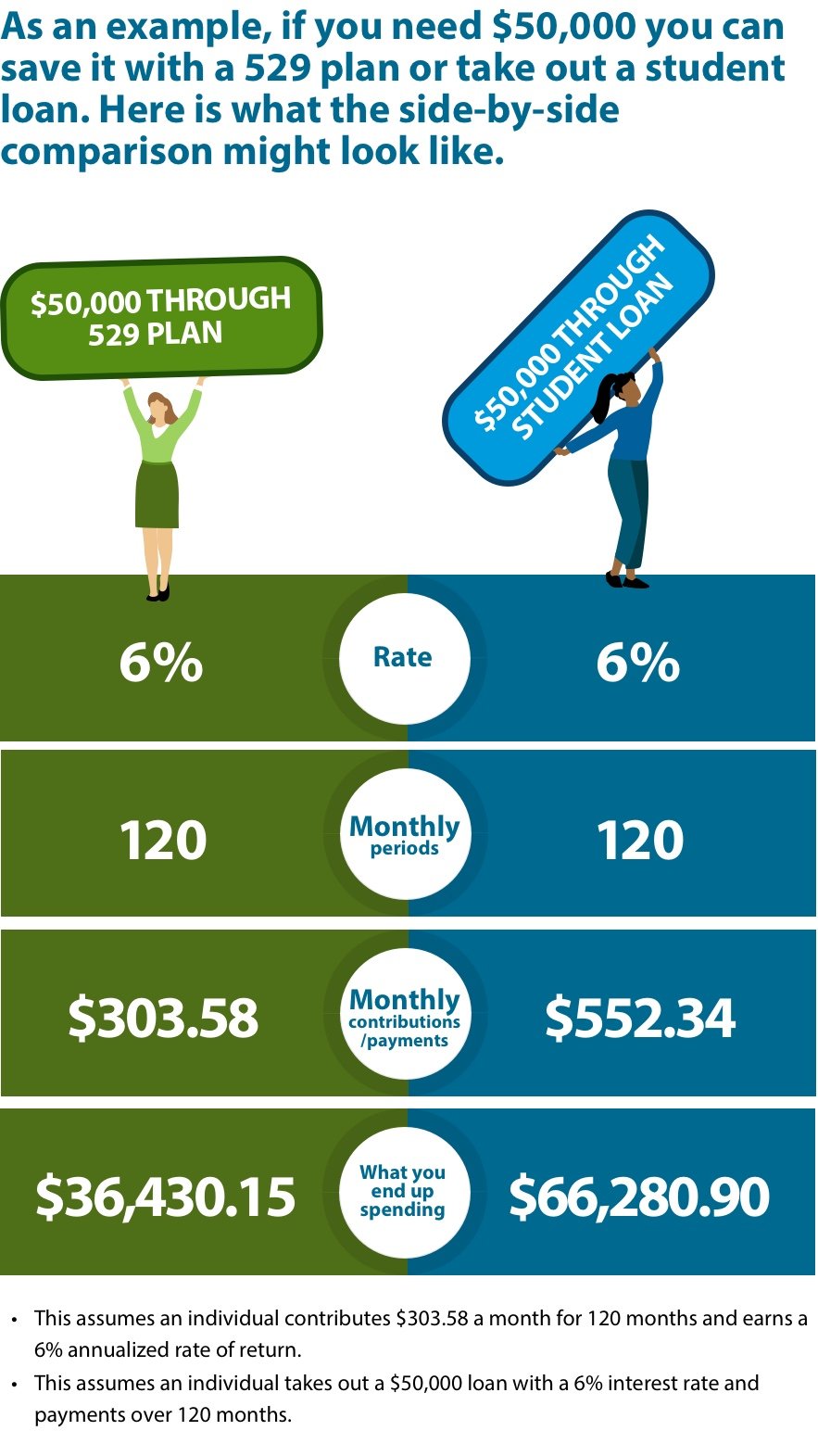

If you’re a parent, chances are, you worry a little. Okay, maybe more than a little. But saving for college shouldn’t be something that keeps you up at night. There are smart ways to save for college – and set your child up for success. In most cases, your 529 plan will have a minimal effect on the amount of aid you receive and will end up helping you more than hurting you. In fact, the benefits of saving now far outweigh relying on financial aid later.

Take 529 plans, for example. These are state-sponsored savings plans that are easy to open and designed to pay for future education expenses.

But before we go further .... What is a 529 plan?

It’s a tax-advantaged savings plan that can help you put away money for your child’s future education costs. If you’re not familiar with a 529 plan, you’re not alone. Your parents may or may not have known about them when they were saving for your college costs.

In short, a 529 plan may be one of the best ways to save for your child’s future education because it offers key tax advantages:

- Tax-deferred earnings: You don’t have to pay federal income taxes on your earnings while in a 529 plan.

- Tax-free withdrawals: When you take money out of a 529 plan to pay for qualified education expenses, you don’t have to pay federal income taxes on it.

- Possible tax deductions: Some states offer additional tax incentives such as deductions, credits or a small additional contribution to the plan.

The key here is that the money must be used to pay for qualified education expenses. No, you can’t use it to pay for a vacation, furniture, or to settle old credit card debt without paying extra. To keep it tax-free, you must use the funds for tuition and fees, room and board (if the student is enrolled at least half time), books and supplies, or computers and education technology at an eligible institution. For a full list of qualified education expenses refer to the current IRS guidelines.

If your child doesn’t attend traditional college, you can also use the funds strategically. You don’t have to worry that the money will “go to waste.” For example, you can withdraw money to:

- Pay off student loans. You can withdraw up to $10,000, without paying federal taxes or penalties.

- Support another college-bound family member. It’s easy to transfer 529 account beneficiaries. If you’ve been saving for one child who doesn’t need the funds, switching beneficiaries to a sibling is easy. You or your spouse can also use the funds to further your education. Nice!

- Pay for K-12 private school. If you have younger children, you can withdraw funds tax-free to help pay for K-12 tuition and fees at qualified private schools.

- Help fund a Roth IRA. Most recently, the law changed so that you can roll over 529 funds into a Roth IRA for the beneficiary. If college isn’t the plan now, no problem. You can always use the money to help support your child later in life.

The bottom line: Even if your child is unsure about going to college now, it’s smart to save. The money can be used for many purposes, whether it’s trade school, college a few years down the road, or to support another family member in need.

According to Chuck Simms, Products Director at Modern Woodmen, it’s worth it to save money now, even if you’re not sure if your child will attend traditional college. “You don’t want your child to be in their early 20s and crushed under a pile of debt. Saving in a 529 account now, even if it’s just a little bit per month, can help protect your child from financial burden of larger loan repayments later on in life,” says Simms.

As a parent, one of the most caring things you can do is put away money to help reduce student loan debt. This can help build a foundation to set your child up for success, enabling them to pursue life goals with less financial burden as they are starting out. Even if they don’t attend college, there are many other creative ways to use the funds and help your child (or a sibling) get ahead.

What’s the most common type of 529 plan, and how does it work?

The most common type of 529 is a college savings plan, which grows through various investment options. Typically, these plans are invested in mutual funds, so you have the ability to select a fund that fits your risk tolerance. Modern Woodmen financial representatives can help you determine which funds are within your risk tolerance so you can grow your portfolio in a way that is comfortable to you and helps you achieve your stated goals.

Next, it’s the question most people ask – does a 529 plan impact financial aid? As we mentioned, the impact is minimal and it’s definitely not a reason to avoid saving for education. In fact, a parent-owned 529 plan only reduces financial aid by a maximum 5.64% of the account’s value.1* We’ll explain.

First, when students apply for financial aid, they fill out a FAFSA, which stands for Free Application for Federal Student Aid. This form helps the government determine if your child qualifies for federal financial aid, and if so, how much they should receive. Federal financial aid can come in the form of grants, loans, and work-study assignments.

One of the most important things to know about the FAFSA is that it helps the government understand your Student Aid Index (SAI), previously called the Expected Family Contribution (EFC), and therefore, your child’s financial need. Any accounts under your child’s name, including 529 plans, can potentially reduce the amount of aid your child receives.

But don’t worry, this isn’t a reason to delay opening a 529 plan or avoid one altogether.

It’s never too late to start saving in a 529 plan

Modern Woodmen financial representatives will talk to you about the benefits of saving for college now, even if your child is already in high school and you’re worried it’s too late.

Trust us, it’s never too late. Even if you don’t start saving until your child is in their teens and only save $10,000, it’s still better than not saving at all. Again, a 529 plan only reduces financial aid by 5.64% of the account’s value.1 Just think. If you have $10,000 in the account, that’s just a $564 reduction in need-based aid. The benefit of saving in a 529 far outweighs any hit on your child’s aid.

Stay connected to experts and keep saving

Remember, laws that relate to 529 plans can change quickly. It’s important to stay connected to a financial professional who can brief you on the latest guidelines and recommendations. Modern Woodmen is here for you throughout every stage of life, from growing your family to saving for college and all the years beyond. Talk to a Modern Woodmen financial representative today to learn more about navigating your college savings options.

1https://www.savingforcollege.com/article/yes-your-529-plan-will-affect-financial-aid

*Consider the investment objectives and risks and the charges and expenses of the investment company carefully before investing. Investments in 529s and mutual funds are subject to market risks, including the potential loss of principal. For this and other information about the investment company, obtain a prospectus from your Modern Woodmen representative. Read it carefully before you invest or pay money. Securities offered through MWA Financial Services, Inc., a wholly owned subsidiary of Modern Woodmen of America. Member: FINRA, SIPC